Imagine this scenario: You’re browsing homes for sale, crunching numbers to determine what you can comfortably afford each month…but what if there was a way to make those mortgage payments more manageable? Enter: weekly mortgage payments.

Instead of shelling out a larger sum once a month, you’d be making four smaller installments every seven days. Sounds intriguing, doesn’t it? Not only could this approach make budgeting easier, but it might also save you a tidy sum in interest over the life of the loan.

So, what exactly are weekly mortgage payments, and are they a viable option for you? Let’s dive in and explore the nitty-gritty details of this increasingly popular payment plan, including the pros, cons, and key considerations to keep in mind.

What Are Weekly Mortgage Payments?

At its core, a weekly mortgage payment plan involves dividing your monthly mortgage obligation by four and paying that amount every seven days. For example, if your monthly payment is $1,200, you’d pay $300 each week instead of the full $1,200 once a month. Simple enough, right?

While this option isn’t universally available from all lenders, it’s becoming increasingly common, particularly for VA loans backed by the U.S. Department of Veterans Affairs. As more lenders recognize the potential benefits for borrowers, we may see wider adoption of weekly payment plans in the future.

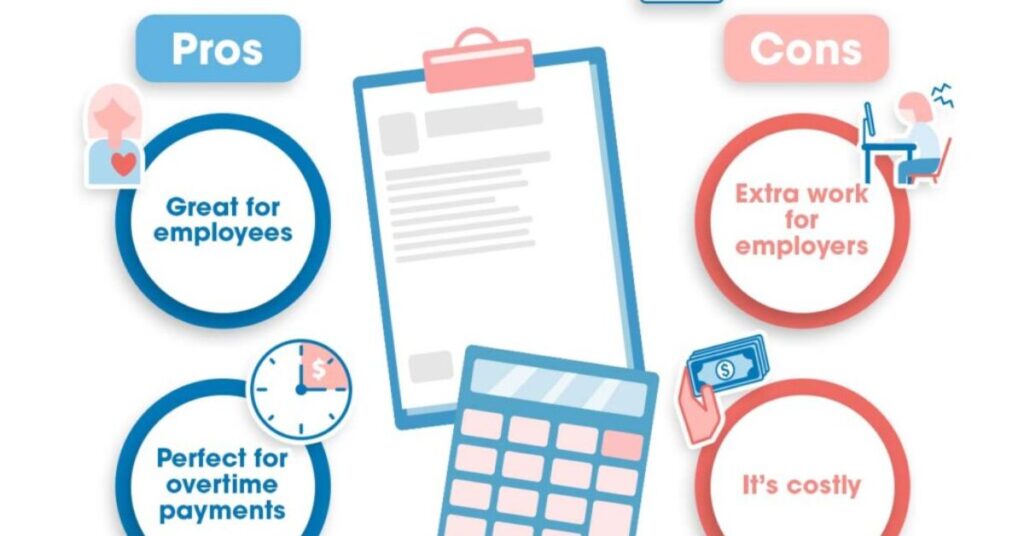

The Pros of Weekly Payments

Now that we’ve covered the basics, let’s explore some of the key advantages that weekly mortgage payments can offer:

- Smaller, More Manageable Payments: Instead of one larger monthly sum, you’re dividing that amount into four smaller installments. For many homeowners, these bite-sized payments can be easier to budget for and less of a strain on their cash flow.

- Interest Savings Over Time: By making more frequent payments throughout the month, you’re effectively reducing the outstanding principal balance a bit quicker. And the sooner you can chip away at that principal, the less interest you’ll pay over the life of the loan.

- Potential to Pay Off the Mortgage Faster: Building on the previous point, those interest savings can add up, potentially allowing you to pay off your mortgage ahead of schedule – without any extra effort on your part.

- Chance to Get Ahead if Extra Payments Made: If you have some extra cash to spare, making an additional weekly payment here and there can give you a head start on reducing that principal balance even quicker.

Let’s dig a little deeper into that interest savings aspect. According to research from the Consumer Financial Protection Bureau, a homeowner with a 30-year, $200,000 mortgage at 4% interest could save over $27,000 in interest by making biweekly (or weekly) payments instead of monthly installments. That’s a substantial amount of money that could be better invested elsewhere or put toward other financial goals.

Potential Downsides to Consider

Of course, no payment plan is perfect, and weekly mortgage payments do come with a few potential drawbacks to keep in mind:

- Missing a Payment Can Put You Behind Quickly: With monthly payments, you essentially have a 30-day grace period before you’re considered late. But when you’re making payments every seven days, falling behind can happen much faster – missing just one installment means you’re automatically 25% delinquent for that month.

- Need to Ensure Sufficient Cash Flow: While the individual payments may be smaller, you’ll need to have enough consistent cash flow to make those weekly contributions without fail. Any disruptions in income could make it challenging to keep up.

- Potential Fees from Some Lenders: Certain lenders may charge additional fees for setting up or maintaining a weekly payment plan, which could offset some of the interest savings you’d accrue.

However, it’s important to note that for many homeowners, the advantages of weekly payments often outweigh these potential downsides. As long as you’re diligent about making those frequent installments and your lender doesn’t impose excessive fees, the interest savings alone could make this approach worthwhile.

Is It Right for You? Factors to Weigh

At the end of the day, weekly mortgage payments aren’t an ideal fit for everyone. Before committing to this payment plan, it’s crucial to carefully evaluate your unique financial situation and consider factors like:

- Personal Cash Flow and Budgeting Preferences: Do you have a steady stream of income that could accommodate weekly installments? Or would a monthly payment better align with your typical cash flow cycles? Consider your comfort level with budgeting for frequent, smaller payments versus one larger sum each month.

- Whether You Plan to Make Additional Payments: If you’re hoping to make extra payments beyond the minimum to pay down your mortgage faster, a weekly plan could be a strategic choice. Those additional installments would accelerate your progress even further.

- Loan Terms and Associated Fees from Your Lender: Review the specific terms of your mortgage, including any fees your lender might charge for setting up or maintaining a weekly payment plan. Ensure that the potential interest savings justify those additional costs.

To illustrate these considerations, let’s look at a couple of hypothetical scenarios:

- The Salaried Professional: Jane is a marketing manager with a stable, salaried income. She prefers to automate her finances as much as possible and appreciates the predictability of set monthly payments. In her case, a traditional monthly mortgage payment might be the more straightforward and comfortable approach.

- The Freelance Consultant: On the other hand, Mike is a freelance consultant with variable monthly income streams. He’s diligent about budgeting and prefers to break down larger expenses into smaller increments. Additionally, Mike hopes to pay off his mortgage early by making extra payments whenever possible. For someone like Mike, a weekly payment plan could be an excellent fit, allowing him to align his mortgage contributions with his cash flow while accelerating his payoff timeline.

As these examples illustrate, there’s no one-size-fits-all solution. The key is to carefully assess your financial dynamics and long-term goals to determine if weekly mortgage payments could be a practical, money-saving strategy for you.

Setting Up Weekly Payments

If you’ve weighed the pros and cons and decided that a weekly payment plan aligns with your priorities, the next step is to explore setting it up with your lender. Here’s a typical process you might encounter:

- Check if Your Lender Offers Weekly Payments: Not all mortgage providers offer this option, so your first step should be to inquire with your lender about their policies and requirements for weekly installments.

- Discuss Setting It Up During the Closing Process: If you’re applying for a new mortgage, you can often indicate your preference for weekly payments during the closing process. Your lender will walk you through the specifics and any associated fees or documentation needed.

- Decide if You’ll Pay via Automatic Bank Transfers: To avoid any missed installments, many homeowners opt to set up automatic weekly transfers from their checking account to the mortgage servicer. This approach ensures timely payments without any manual effort on your part.

Pro Tip: Regardless of whether you choose automatic payments or prefer to initiate the transfers manually, setting up calendar reminders or alerts can be a helpful safeguard against accidentally skipping a weekly installment.

Signs Weekly Payments Are Working

Once you’ve transitioned to a weekly mortgage payment plan, there are a few telltale signs that this approach is paying off (literally!):

- Payments Feel More Manageable: Instead of that looming monthly bill, you’re chipping away at your mortgage balance in smaller, more digestible increments. This can alleviate some of the financial stress and strain often associated with larger, infrequent payments.

- Seeing the Mortgage Balance Dwindle Faster: Thanks to the frequent installments, you’ll likely notice your outstanding principal balance decreasing at a slightly quicker pace compared to a traditional monthly payment schedule.

- Interest Savings Adding Up Over Time: As mentioned earlier, the more you can reduce that principal balance, the less interest you’ll ultimately pay over the life of the loan. These savings may start small, but they can compound into a substantial amount by the time you’ve paid off your mortgage.

Conclusion

Weekly mortgage payments offer a compelling alternative to traditional monthly installments, providing potential interest savings, quicker principal paydown, and more manageable cash flow for many homeowners.

However, this approach isn’t a universal solution its viability depends on factors like your income stability, budgeting preferences, and willingness to make frequent payments. By carefully evaluating your financial situation and weighing the pros and cons, you can determine if weekly installments align with your goals.

Those who do opt for this route may enjoy substantial long term savings, accelerated debt repayment, and the peace of mind that comes with breaking down a larger obligation into smaller, more digestible chunks.

Ultimately, exploring all available mortgage payment strategies empowers you to make an informed decision that optimizes your hard earned money and sets you on a path toward lasting financial security.

“Meet Alena Genefair, a seasoned finance expert with over five years of experience and the esteemed author behind FinanceHookup. With a wealth of knowledge in financial management, investment strategies, mortgages, and banking, Alena provides insightful perspectives to readers. Her expertise helps individuals navigate the complexities of personal finance with clarity and confidence.”