In today’s digital age, plastic cards and virtual wallets have largely replaced cash. Yet, many of us still scratch our heads when we see POS debit or point of sale charges on our bank statements. What are these mysterious entries? How do they affect our finances? Let’s dive deep into the world of POS transactions and unravel the complexities of modern-day purchases.

What Are POS Debit and Point of Sale Charges?

POS, short for Point of Sale, refers to the place where a retail transaction occurs. This could be a physical cash register at your local grocery store or a virtual checkout page on an e-commerce website. When you use your debit card or credit card at these points, you’re making a POS transaction.

A POS debit charge specifically refers to a transaction where funds are directly withdrawn from your checking account. On the other hand, a POS charge using a credit card doesn’t immediately affect your bank balance but adds to your credit card bill.

The Anatomy of a POS Transaction

- You swipe, dip, or tap your card at the point-of-sale system.

- The payment processor verifies your card details.

- Your bank confirms you have sufficient funds.

- The transaction is approved, and funds are transferred.

- You receive a receipt, and the merchant gets paid.

This process happens in seconds, showcasing the marvels of modern financial technology.

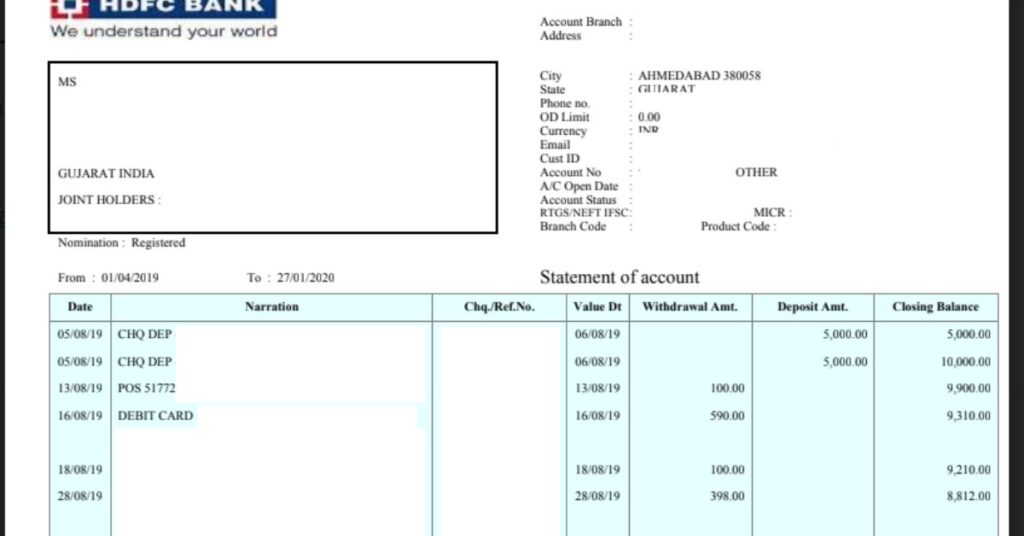

Decoding Your Bank Statement: POS Debit Demystified

When you look at your bank statement, you might see entries like “POS DBT PURCHASE” or “POS WITHDRAWAL.” These descriptors can be confusing, but they’re simply different ways of saying you made a purchase using your debit card at a point of sale.

Here’s a quick guide to common POS-related terms you might encounter:

| Term | Meaning |

| POS DBT | Point of Sale Debit |

| POS WDL | Point of Sale Withdrawal |

| POS CRD | Point of Sale Credit (for credit card transactions) |

| EFTPOS | Electronic Funds Transfer at Point of Sale |

Understanding these terms can help you better track your spending and spot any suspicious activity.

The Mechanics Behind POS Debit Transactions

Let’s break down what happens behind the scenes when you make a POS debit transaction:

- Card Presentation: You present your debit card at the point of sale.

- Data Transmission: The merchant’s POS system sends your card data to their bank.

- Authorization Request: The merchant’s bank forwards this request to your bank.

- Verification: Your bank checks if you have sufficient funds.

- Response: Your bank sends an approval or denial back through the chain.

- Completion: If approved, the transaction is completed, and you receive a receipt.

This process involves multiple parties, including you (the customer), the merchant, both banks, and the payment network (like Visa or Mastercard).

Types of POS Charges You Might Encounter

Not all POS charges are created equal. Here are some variations you might see:

- Standard POS Debit: The most common type, where funds are immediately deducted from your account.

- POS Credit: When you use a credit card at a point of sale.

- International POS: Charges made in foreign countries, often incurring additional fees.

- Cash Back at POS: When you request cash along with your purchase.

Each of these can appear differently on your statement, so it’s crucial to familiarize yourself with the various descriptors.

Pros and Cons of POS Debit Transactions

Like any financial tool, POS debit transactions have their advantages and drawbacks.

Pros:

- Immediate: Transactions are processed in real-time.

- Budgeting: Helps you stick to your budget as you can’t spend more than you have.

- Widely Accepted: Most merchants accept debit cards.

- Lower Fees: Generally incur fewer fees than credit cards.

Cons:

- Overdraft Risk: You might overdraw your account if you’re not careful.

- Less Protection: May offer fewer fraud protections compared to credit cards.

- Holds on Funds: Some merchants may place holds on your account, temporarily reducing your available balance.

POS Debit Fees: What to Watch Out For

While POS debit transactions are often free for consumers, there are scenarios where you might incur fees:

- Out-of-Network ATM Fees: If you use your debit card at an ATM outside your bank’s network.

- Foreign Transaction Fees: When making purchases abroad or in foreign currencies.

- Overdraft Fees: If you spend more than your account balance.

- Merchant Surcharges: Some businesses charge extra for debit card use, though this is becoming less common.

“Knowledge is power. Understanding the fees associated with your transactions can save you a significant amount of money over time.” – Financial expert Jane Doe

Securing Your POS Debit Transactions

In an era of increasing digital fraud, securing your POS debit transactions is crucial. Here are some best practices:

- Guard Your PIN: Never share your PIN or write it down.

- Use Chip and PIN: Chip transactions are more secure than magnetic stripe.

- Monitor Your Statements: Regularly check for unauthorized transactions.

- Use Secure Networks: Avoid making online purchases on public Wi-Fi.

- Enable Notifications: Set up alerts for all transactions on your account.

Case Study: The Impact of POS Debit on Small Businesses

Let’s look at how POS debit transactions affect both consumers and businesses:

Joe’s Coffee Shop implemented a modern POS system that accepts debit cards. Here’s what happened:

- Customer Convenience: Customers appreciated the ability to pay with cards, leading to increased satisfaction.

- Higher Sales: Average transaction value increased by 15% as customers weren’t limited by the cash in their wallets.

- Faster Transactions: Checkout times decreased, improving overall efficiency.

- Better Record-Keeping: The digital system made bookkeeping easier and more accurate.

However, Joe had to factor in transaction fees, which slightly reduced his profit margins. Despite this, the benefits outweighed the costs, demonstrating the value of embracing POS debit technology for both businesses and consumers.

The Future of POS Debit and Point of Sale Charges

As technology evolves, so do our payment systems. Here’s what we might expect in the coming years:

- Contactless Payments: The rise of NFC technology is making tap-to-pay more common.

- Mobile Payments: Smartphones are increasingly being used as payment devices.

- Biometric Authentication: Fingerprint or facial recognition might replace PINs.

- Blockchain and Cryptocurrencies: These could revolutionize how we think about POS transactions.

Conclusion: Empowering Consumers in the POS Debit Era

Understanding POS debit and point of sale charges is crucial in today’s digital economy. By demystifying these transactions, we empower ourselves to make informed financial decisions, spot discrepancies, and use our debit cards more effectively.

Remember:

- Regularly review your bank statements

- Understand the different types of POS charges

- Be aware of potential fees

- Prioritize security in all your transactions

By staying informed and vigilant, you can navigate the world of POS debit with confidence, making the most of this convenient payment method while protecting your financial health.

FAQs About POS Debit and Point of Sale Charges

- What’s the difference between a POS debit and an ATM withdrawal?

- POS debit occurs when you make a purchase, while an ATM withdrawal is purely for obtaining cash.

- Can I dispute a POS charge?

- Yes, you can dispute unauthorized or incorrect charges with your bank.

- Are POS debit transactions instant?

- While the approval is instant, the actual transfer of funds can take 1-3 business days to fully process.

- How can I tell if a POS charge is fraudulent?

- Look for unfamiliar merchant names, unusual amounts, or transactions in locations you haven’t visited.

- Do all merchants accept POS debit transactions?

- While most do, some small businesses or market vendors might be cash-only. Always check before making a purchase.

By understanding POS debit and point of sale charges, you’re taking a significant step towards better financial management. Stay informed, stay secure, and make the most of your debit card transactions!

“Meet Alena Genefair, a seasoned finance expert with over five years of experience and the esteemed author behind FinanceHookup. With a wealth of knowledge in financial management, investment strategies, mortgages, and banking, Alena provides insightful perspectives to readers. Her expertise helps individuals navigate the complexities of personal finance with clarity and confidence.”