As you approach your golden years, ensuring a comfortable retirement becomes a top priority. One option that has gained traction is the lifetime mortgage, which allows you to access the equity tied up in your home without having to sell or move out. But what exactly is a lifetime mortgage, and is it the right choice for you? Let’s dive in and explore this increasingly popular financial tool.

What Exactly is a Lifetime Mortgage?

At its core, a lifetime mortgage is a type of equity release scheme that enables homeowners aged 55 or older to access a portion of their home’s value as tax-free cash. Think of it as a loan secured against your property, but unlike a traditional mortgage, you don’t have to make any monthly repayments. Instead, the loan amount, plus interest, is repaid when you pass away or move into long-term care, usually by selling the property.

To illustrate, imagine your home is currently worth $400,000, and you have no outstanding mortgage. With a lifetime mortgage, you could potentially borrow up to 50% of that value (around $200,000) as a lump sum or a series of smaller withdrawals. This money is yours to use however you see fit, whether it’s supplementing your retirement income, funding home renovations, or simply enjoying your golden years to the fullest.

How Does a Lifetime Mortgage Work?

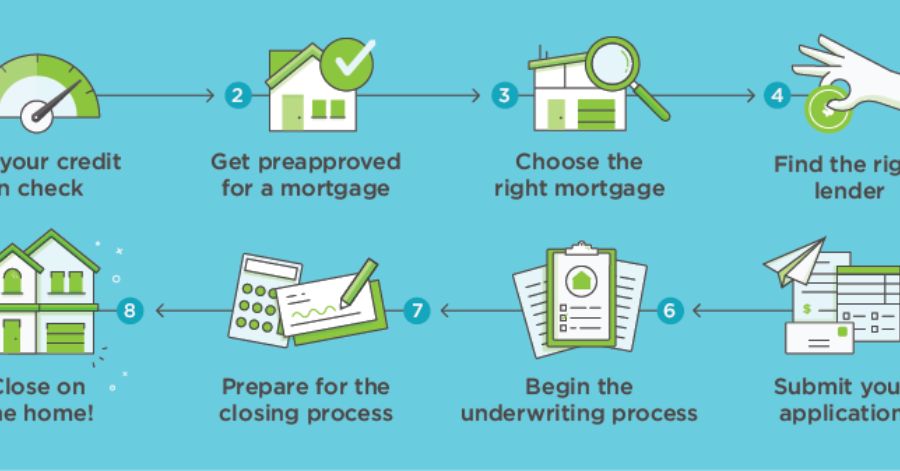

The process of obtaining a lifetime mortgage typically involves the following steps:

- Eligibility Check: Lenders will assess your age, home value, and overall financial situation to determine if you qualify for the scheme.

- Property Valuation: An independent surveyor will visit your home to provide an accurate property appraisal and ensure it meets the lender’s criteria.

- Loan Calculation: Based on your age, property value, and the lender’s terms, the maximum loan amount you can borrow will be calculated.

- Loan Setup: If you decide to proceed, you’ll need to complete the application process and pay any associated fees and lending costs.

- Funds Release: Once approved, the lender will release the agreed equity withdrawal amount to you as a lump sum or in smaller installments (known as a drawdown facility).

- Interest Accrual: Interest on the loan will begin accruing from the day you receive the funds, compounding over time.

- Loan Repayment: The loan, plus accumulated interest, becomes due when you pass away or move into permanent care, typically repaid by selling the property.

It’s important to note that with a lifetime mortgage, you retain full ownership of your home and can continue living there for the rest of your life, provided you adhere to the terms of the agreement.

Eligibility Requirements for a Lifetime Mortgage

While specific requirements may vary between lenders, here are some common eligibility criteria for a lifetime mortgage:

- Age: You must be at least 55 years old (sometimes 60 or 65 for certain plans).

- Property Value: Your home must meet the lender’s minimum value threshold, often around $100,000 or more.

- Property Type: Typically, only standard residential properties are eligible (no mobile homes or houseboats).

- Property Condition: Your home should be in a reasonable state of repair and meet basic lending criteria.

- Residency Status: You must be a permanent resident or citizen of the country where the property is located.

It’s essential to consult with a reputable financial adviser or mortgage consultant to ensure you fully understand the eligibility requirements and potential implications of a lifetime mortgage for your specific situation.

Types of Lifetime Mortgages

There are two main types of lifetime mortgages available:

- Lump Sum Lifetime Mortgage

- You receive the entire loan amount as a single, upfront payment.

- Ideal for those with immediate, larger expenses (e.g., debt consolidation, home renovations).

- Interest accrues on the full loan amount from day one.

- Drawdown Lifetime Mortgage (also known as Flexible Cash Reserve)

- You receive an initial lump sum, with the option to access additional funds as needed.

- Designed for those who want access to funds gradually over time.

- Interest is only charged on the amount you’ve withdrawn, not the full approved limit.

- Offers more flexibility but may have higher setup costs.

Both options typically feature a no negative equity guarantee, ensuring you’ll never owe more than the value of your home when the loan is repaid. However, it’s crucial to weigh the pros and cons of each type carefully with the guidance of a financial professional.

Advantages of a Lifetime Mortgage

Lifetime mortgages offer several potential benefits that make them an attractive option for many homeowners:

- No Monthly Payments: Unlike a traditional mortgage or home equity loan, you don’t have to make any monthly repayments with a lifetime mortgage. This can help alleviate financial strain during retirement.

- Retain Home Ownership: With a lifetime mortgage, you remain the legal owner of your property and can continue living there for the rest of your life, provided you maintain the property and comply with the terms of the agreement.

- Tax-Free Cash: The funds you receive from a lifetime mortgage are generally tax-free, as they are considered a loan rather than income.

- Flexible Use of Funds: You can use the cash from a lifetime mortgage however you see fit, whether it’s for home renovations, medical expenses, travel, or supplementing your retirement income.

- No Repayments During Your Lifetime: The loan and accrued interest are typically repaid when you pass away or move into long-term care, usually by selling the property.

- Potential Tax Benefits: In some cases, a lifetime mortgage may help reduce your overall tax liability or preserve your eligibility for certain government benefits. However, it’s essential to consult a qualified tax professional for personalized advice.

Potential Downsides to Consider

While lifetime mortgages offer several advantages, it’s crucial to understand the potential drawbacks and carefully assess your specific circumstances:

- Reduced Inheritance for Beneficiaries: Since the loan and interest are repaid from the sale of your property, there may be less (or no) equity left to pass on as an inheritance.

- Compound Interest Impact: Interest on a lifetime mortgage compounds over time, potentially reducing the remaining equity in your home at a faster rate than expected.

- Costly Setup and Interest Rates: Lifetime mortgages often have higher setup fees and interest rates compared to traditional mortgages or home equity loans.

- Impacts on Government Benefits: In some cases, the funds received from a lifetime mortgage may affect your eligibility for means-tested government benefits or assistance programs.

- Early Repayment Penalties: Some lifetime mortgage plans may impose penalties or fees if you decide to repay the loan early or sell your home within a certain timeframe.

It’s crucial to carefully consider these potential drawbacks and discuss them with a qualified financial advisor or mortgage consultant to determine if a lifetime mortgage aligns with your long-term goals and financial situation.

Is a Lifetime Mortgage Right for You?

When evaluating whether a lifetime mortgage is the right choice, consider the following questions:

- Do you have a specific need or expense that requires access to additional funds?

- Are you comfortable with the idea of reducing the equity in your home over time?

- Have you explored alternative options, such as downsizing or traditional mortgages/loans?

- Will a lifetime mortgage negatively impact your eligibility for government benefits or your overall tax liability?

- Do you plan to leave an inheritance for your beneficiaries, and if so, how important is preserving that inheritance?

- Are you prepared for the potential impact on your credit score or overall borrowing health?

Ultimately, a lifetime mortgage can be a valuable tool for some homeowners, but it may not be suitable for everyone. It’s crucial to seek professional guidance from a reputable financial advisor or mortgage consultant to ensure you fully understand the implications and make an informed decision based on your unique circumstances.

How to Qualify and Apply for a Lifetime Mortgage

If you’ve carefully considered the pros and cons and decided that a lifetime mortgage aligns with your goals, here are the typical steps to qualify and apply:

- Eligibility Check: Contact several reputable lifetime mortgage lenders and provide basic information about your age, property details, and financial situation to determine if you meet their eligibility criteria.

- Property Valuation: Once you’ve identified potential lenders, they will arrange for an independent surveyor to visit your home and conduct a thorough property assessment to determine its current market value.

- Application Process: If you meet the lender’s requirements and are satisfied with the property valuation, you’ll need to complete a formal application, providing detailed financial information, identification documents, and any other required paperwork.

- Credit and Affordability Check: The lender will

a credit check and assess your overall financial situation to ensure you can afford the lifetime mortgage and meet their lending criteria.

- Loan Offer: If your application is approved, the lender will provide you with a loan offer detailing the maximum loan amount, interest rates, fees, and terms of the agreement.

- Legal Review: It’s crucial to have an independent legal professional review the loan offer and associated documents to ensure you fully understand the terms and implications before proceeding.

- Completion: Once you’ve accepted the loan offer and completed any remaining requirements, the lender will release the agreed funds to you, either as a lump sum or through a drawdown facility.

Throughout the application process, it’s essential to be transparent about your financial situation and ask questions if anything is unclear. Additionally, don’t hesitate to shop around and compare offers from multiple reputable lenders to ensure you’re getting the best terms and rates available.

Closing Thoughts

A lifetime mortgage can be a valuable financial tool for homeowners aged 55 and older, providing access to tax-free cash from the equity tied up in their property. However, it’s a significant financial decision that should not be taken lightly.

While a lifetime mortgage offers several advantages, such as no monthly repayments and the ability to retain home ownership, it also comes with potential drawbacks, including reduced inheritance for beneficiaries, the impact of compounding interest, and costly fees.

Ultimately, the decision to pursue a lifetime mortgage should be based on a thorough understanding of your unique financial situation, goals, and the long-term implications. It’s crucial to consult with qualified professionals, such as financial advisors, mortgage consultants, and legal experts, to ensure you make an informed decision that aligns with your best interests.

Remember, a lifetime mortgage is a lifelong commitment, so take the time to carefully consider all aspects before proceeding. With proper guidance and a clear understanding of the pros and cons, a lifetime mortgage can be a valuable tool for enjoying a more financially secure retirement.