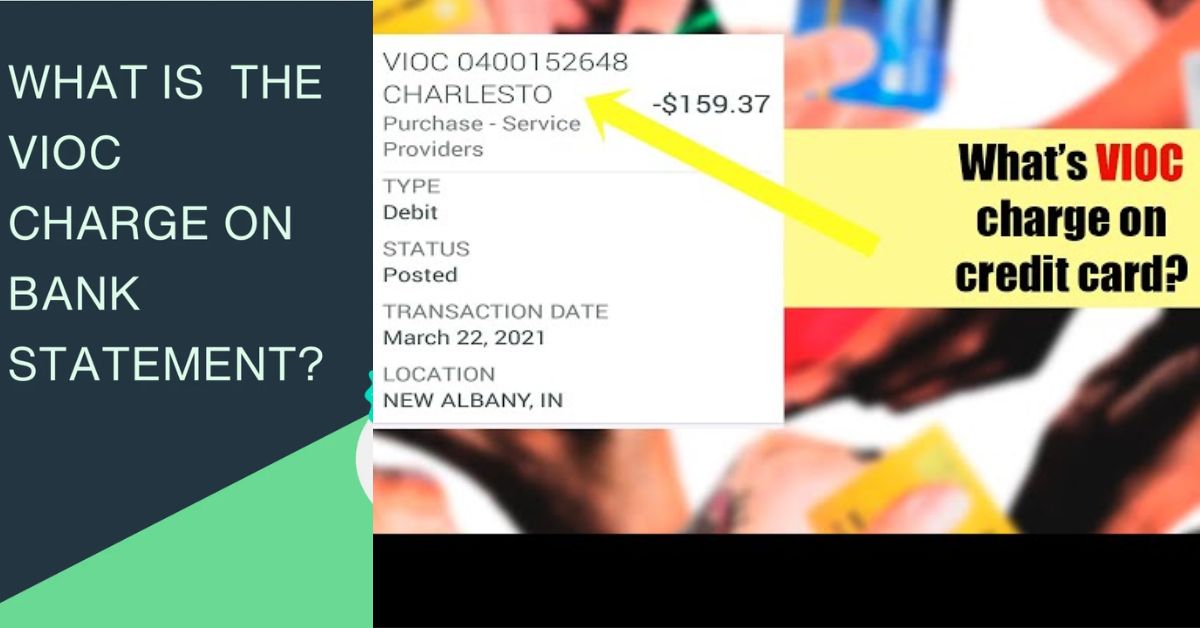

Have you ever noticed an unfamiliar charge on your bank statement with the confusing acronym “VIOC” and wondered what it meant? You’re not alone – this fee, which stands for “Vendor’s Inquiry on Credit,” catches many consumers off guard. In this article, we’ll dive deep into understanding VIOC charges, why they appear, and how to potentially avoid them.

A VIOC charge is a small fee, typically ranging from $0.50 to $1, that gets added to your account when a merchant checks your available credit or funds before completing a transaction.

This allows the merchant to verify that you have sufficient funds or credit limit to cover the purchase, helping them prevent potential losses from bounced payments or declined transactions.

Why Are VIOC Charges Added to Your Account?

While the practice of checking available balances may seem like an unnecessary inconvenience for customers, it serves an important purpose for merchants – protecting them from credit risk. By running these inquiries, known as “VIOC checks,” businesses can ensure they won’t be left holding the bag if a customer’s account doesn’t have adequate funds or credit to cover the full transaction amount.

Some common scenarios where you might see a VIOC charge include:

- Credit card transactions over a certain dollar amount: Many merchants will run a VIOC check for higher-value credit card purchases, with typical thresholds ranging from $50 to $300 depending on the business.

- Recurring subscriptions or membership charges: Companies offering recurring services, like gym memberships or subscription boxes, may do periodic VIOC checks to validate your payment method.

- Hotels, rental car companies, and restaurants: These merchants often do a VIOC check when you arrive to ensure you can cover any potential incidental charges beyond the reserved room, car rental, or meal cost.

While understandable from a business risk perspective, VIOC fees can add up quickly for consumers making several transactions per month – especially if their bank charges closer to the $1 maximum amount.

How Much is a Typical VIOC Fee?

As mentioned, VIOC fees generally range from about $0.50 to $1 per inquiry, though the exact amount can vary between banks and credit card issuers. Here are some examples of common VIOC charge amounts from major U.S. banks:

| Bank | VIOC Fee |

| Bank of America | $0.50 |

| Chase | $0.50 |

| Citi | $0.95 |

| Wells Fargo | $0.20-$1.00 |

While a dollar or less may not seem like much, these small charges can add up quickly if you frequently make purchases or use services that trigger multiple VIOC inquiries per month. It’s important to understand what these charges are so you can account for them in your budget and spending.

When Do Merchants Check for VIOC?

As noted in the previous section, there are a few key situations where merchants are likely to perform a VIOC check on your account:

- Credit card purchases over a set dollar amount: To minimize risk, merchants will often check available credit for charges over $50, $100, $200 or more.

- Recurring subscription services: Companies like Netflix, Amazon Prime, gym memberships, etc. may verify your payment method periodically.

- Hotels, rental cars, and restaurants upon arrival: These merchants check to ensure you can cover incidentals beyond just the reserved room, car rental, or meal cost.

- High-risk purchases: Merchants may scrutinize big-ticket items like vehicles, jewelry, or electronics with VIOC checks.

- First-time or infrequent customers: Businesses are more likely to verify newer customers they don’t have purchasing history with yet.

The exact threshold can vary by merchant, but the underlying goal is the same – preventing potential loss from declined transactions or insufficient funds.

Can You Avoid Getting Hit with VIOC Charges?

While VIOC fees are legally permitted for merchants to charge, that doesn’t make them any less frustrating for consumers. If you’re looking to minimize or avoid these account inquiry charges, here are some tips:

Use Debit Instead of Credit When Possible Unlike credit cards, debit card transactions simply draw directly from your checking account balance – no available credit needs to be verified. Many merchants won’t run a VIOC check for debit purchases.

Keep Tabs on Balances and Available Credit Make a habit of monitoring your credit card statements and checking account balances. Keeping sufficient funds can reduce the likelihood of a merchant needing to verify your ability to cover a charge.

Use Mobile Payment Apps/Digital Wallets

Services like Apple Pay, Google Pay, Venmo and others sometimes bypass certain fees by facilitating transactions directly between banks. VIOC charges may not always apply.

Consider Overdraft Protection or Credit Limit Increases

Having overdraft coverage or a credit limit increase gives you more financial cushion, decreasing the necessity for VIOC checks. Though be wary of related fees for these services.

Speak With Your Bank If VIOC charges are a frequent nuisance, have an honest discussion with your bank about potentially waiving or lowering the fee, especially if you maintain a good account history.

At the end of the day, VIOC fees are within a merchant’s rights to charge as part of their financial risk management process. But consumers can take some proactive steps to reduce the likelihood of racking up these small but pesky charges.

Are VIOC Fees Fair and Legal?

The billion-dollar question: are VIOC charges fair to consumers, or an underhanded nickel-and-diming tactic by merchants? As with many things, there are arguments on both sides of this debate.

The Case For VIOC Fees

From a legal and business operations perspective, banks and credit card issuers are well within their rights to permit merchants to charge VIOC fees. These “account inquiry fees” are regulated as legitimate service charges.

Merchants incur processing costs and take on financial risk by accepting credit card payments that could potentially be declined. VIOC checks help businesses validate transactions ahead of time to avoid losing money from “unsuccessful” charges.

Additionally, many defend these fees as simply the cost of doing business in our modern credit-based economy. Credit card processing as a whole isn’t free, after all. VIOC charges could be viewed as the customer briefly “renting” the merchant’s ability to check available balances – a value-added service, albeit a minor one.

Arguments Against VIOC Fees

On the other hand, consumer advocacy groups and outspoken customers argue that VIOC fees are an excessive and deceptive profit-generator, levied with minimal disclosure and transparency. Core criticisms include:

- VIOC charges make even small purchases more expensive for the customer, despite merchants already paying processing fees on transactions.

- Fees aren’t consistently disclosed upfront in advertised prices, feeling like a misleading hidden charge to many.

- Frequency and total costs of VIOC checks can quickly add up, particularly for consumers with limited funds in the first place.

- Concerns that merchants may be running unnecessary VIOC checks just to tack on more fees, rather than for legitimately verifying payment ability.

- Perception that fees disproportionately nickel-and-dime those living paycheck-to-paycheck and with poor financial literacy.

Frustrated consumers have lodged complaints with the Consumer Financial Protection Bureau and other agencies, arguing the ubiquitous charges amount to excessive “legal fraud.” However, the practice remains strictly regulated but allowed for merchants under current laws.

“VIOC fees are really just a backdoor way to increase profits at the consumer’s expense, because none of these ‘verification services’ provide any value to the customer themselves.”

– Personal finance expert, Dave Ramsey

While VIOC charges generate an estimated $20+ billion annually for merchants, heated debates will likely continue around whether these fees cross the line or simply reflect the realities of an economy operating more and more on credit and digital payments.

Conclusion: Understand and Minimize VIOC Charges

VIOC charges, short for “Vendor’s Inquiry on Credit,” are small but pesky fees that merchants add when checking your available credit or funds prior to completing a transaction. They are intended to help businesses avoid potential loss from bounced payments or insufficient balances.

However frustrating these account inquiry fees may be, they are currently permitted by laws and credit card company policies as a legitimate surcharge to cover a merchant’s credit risk costs. VIOC fees typically range from $0.50 to $1 per check and can rack up quickly if you frequently use credit and make high-value purchases.

While you may not be able to eliminate VIOC charges entirely, you can take steps to reduce their impact:

- Use debit cards or cash instead of credit when possible to bypass credit checks

- Keep close tabs on your balances and credit limits to maintain sufficient funds

- Consider overdraft protection or credit limit increases if manageable

- Use

“Meet Alena Genefair, a seasoned finance expert with over five years of experience and the esteemed author behind FinanceHookup. With a wealth of knowledge in financial management, investment strategies, mortgages, and banking, Alena provides insightful perspectives to readers. Her expertise helps individuals navigate the complexities of personal finance with clarity and confidence.”